Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

It’s true that record levels of home price appreciation have spurred significant equity gains for homeowners over the past few years. As Diana Olick, Real Estate Correspondent at CNBC, says:

“The stunning jump in home values over the course of the Covid-19 pandemic has given U.S. homeowners record amounts of housing wealth.”

That’s great for your home’s value over the last couple of years, but what if you’ve lived in your home for longer than that? You may be wondering how much equity you truly have.

The National Association of Realtors (NAR) has done a study to calculate the typical equity gains over longer spans of time. The data they compiled could be enough to motivate you to move. Just remember, to find out how much equity you have in your specific home, you’ll want to get a professional equity assessment from a trusted real estate advisor.

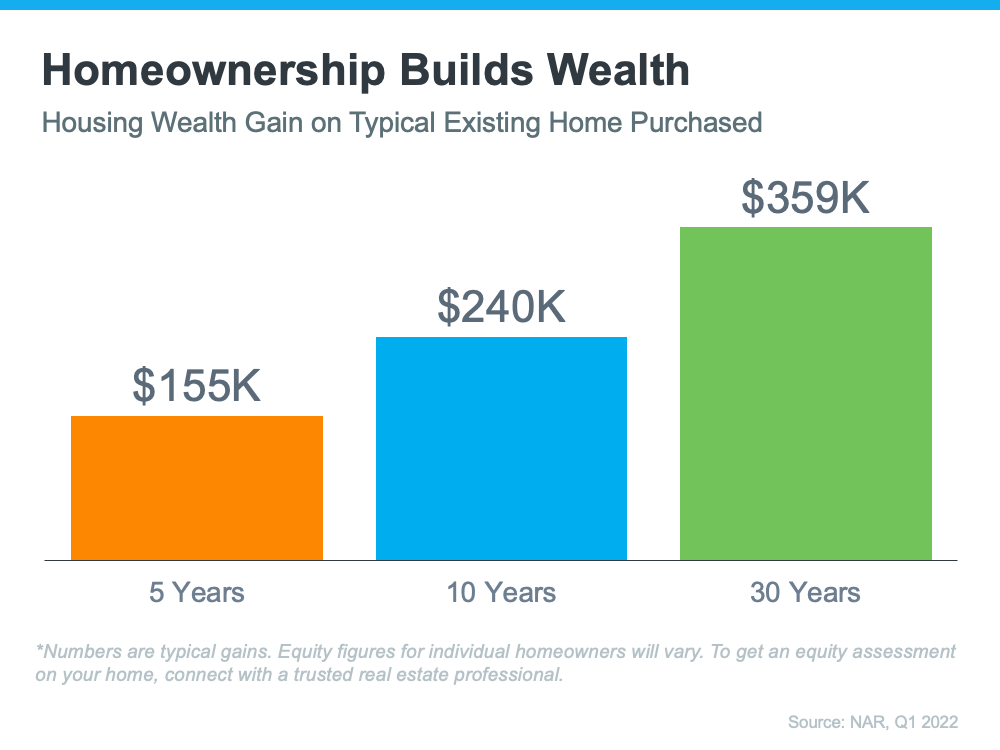

How Your Equity Grows

Let’s start by establishing how you build equity in your home. While price appreciation is clearly a factor that can help boost your equity, you also build equity over time as you pay down your home loan. NAR explains:

“Home equity gains are built up through price appreciation and by paying off the mortgage through principal payments.”

Average Equity Growth over Time

The study from NAR breaks down the typical equity gain over time (see graph below). It calculates the equity a homeowner potentially gained if they purchased the median-priced home 5, 10, or 30 years ago and still own it today.

These six-figure numbers are impressive and certainly enough to help you fuel a move into your next home, but they’re not a promised amount. Remember, your own equity gain will be different. It depends on how long you’ve been in the house, your home’s condition, any upgrades you’ve made, your area, and much more.

If you want to find out how much equity you have, partner with a trusted real estate professional for an equity assessment on your home. They can provide an expert opinion on what your house is worth today and how the equity you’ve gained over time can help you when you purchase your next home. It may be some (if not all) of what you need for your next down payment.

Bottom Line

If you’re thinking about selling your house and making a move, home equity can be a real game-changer, especially if you’ve been in your current home for a while. If you’re ready to find out how much equity you have, let’s connect.

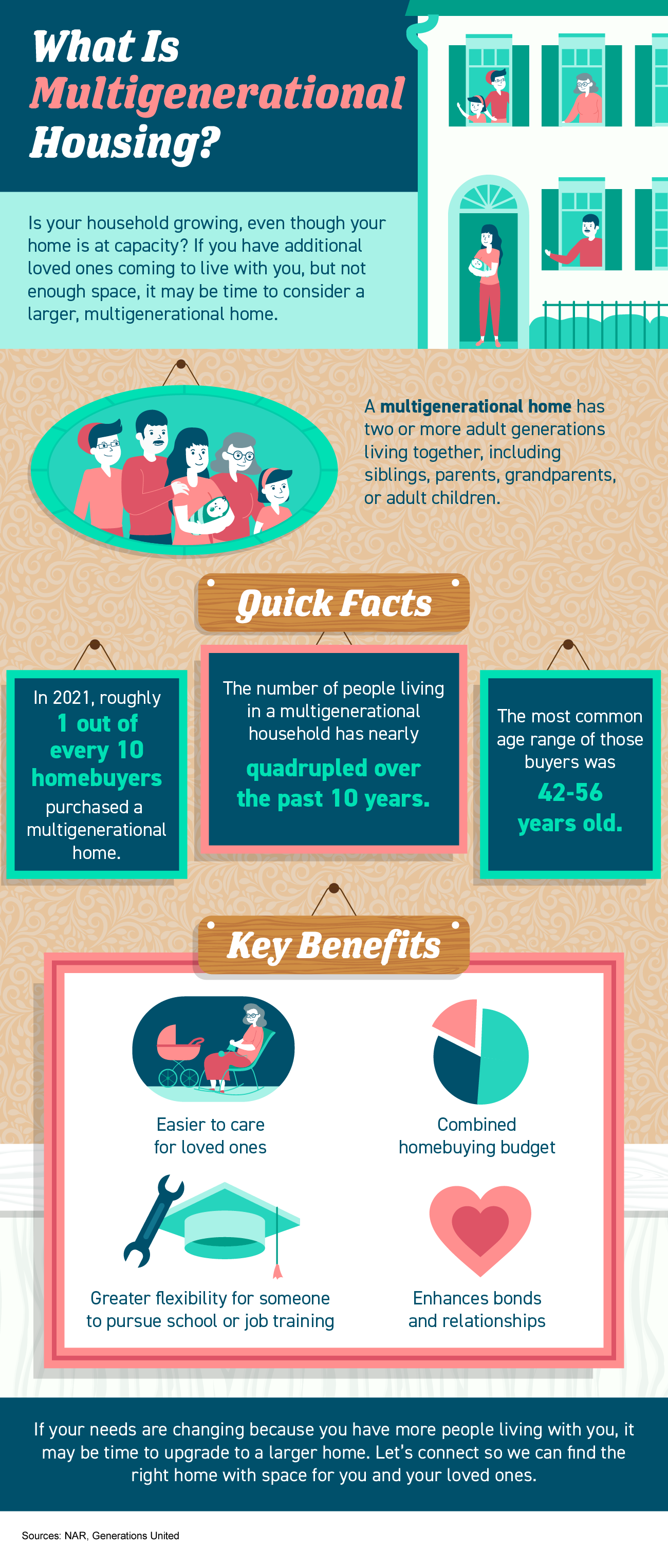

![What Is Multigenerational Housing? [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/04/14144240/20220415-MEM-1046x2456.png)

![Real Estate Consistently Voted Best Investment [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2022/06/30082612/20220701-KCM-Share-549x300.png)

![Real Estate Consistently Voted Best Investment [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2022/06/30082607/20220701-MEM.png)